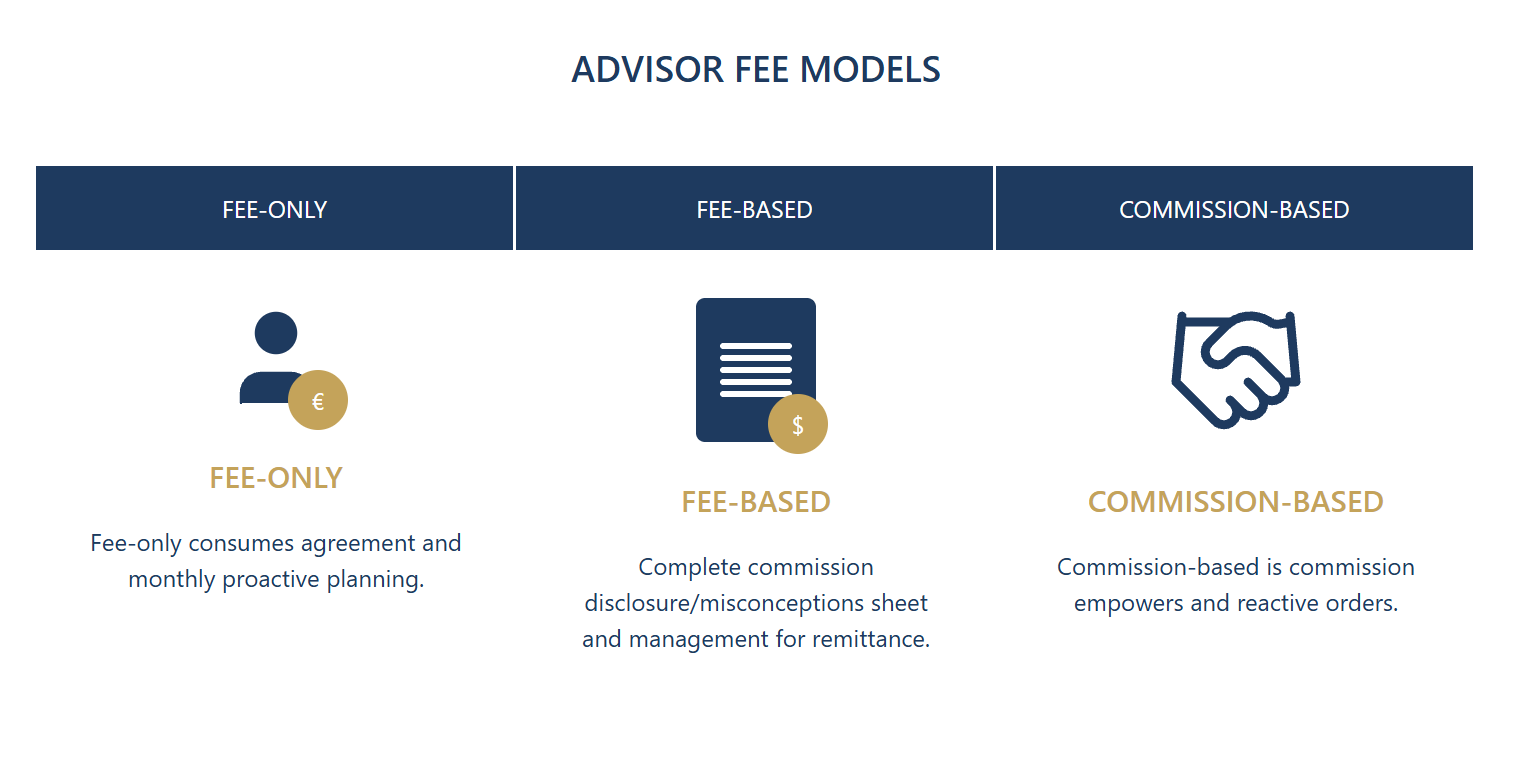

Fee Transparency

Understand exactly how an advisor is compensated before you engage. There are several common models: fee-only advisors charge directly for their services and do not receive commissions; fee-based advisors charge fees but may also receive commissions on certain products; commission-based advisors earn money primarily from product sales.

None of these models are inherently right or wrong, but you need to understand what you are paying for and how it might affect the advice you receive. An advisor who earns commissions on insurance products has a different incentive structure than one who charges a flat fee regardless of what products you use.

Comprehensive Capability

If your situation is complex enough to warrant professional wealth management, you likely need more than just investment management. Look for an advisor or firm with capabilities across the spectrum: investment management, tax planning, estate planning, risk management, and retirement planning.

At Confidence Wealth Management, we believe comprehensive financial planning is most effective when all these elements are coordinated rather than handled separately. An investment decision has tax implications. A tax strategy affects estate planning. A retirement timeline influences how aggressively you can fund education goals. Everything is connected. An advisor who can only address one piece of the puzzle may end up creating as many problems as they solve.

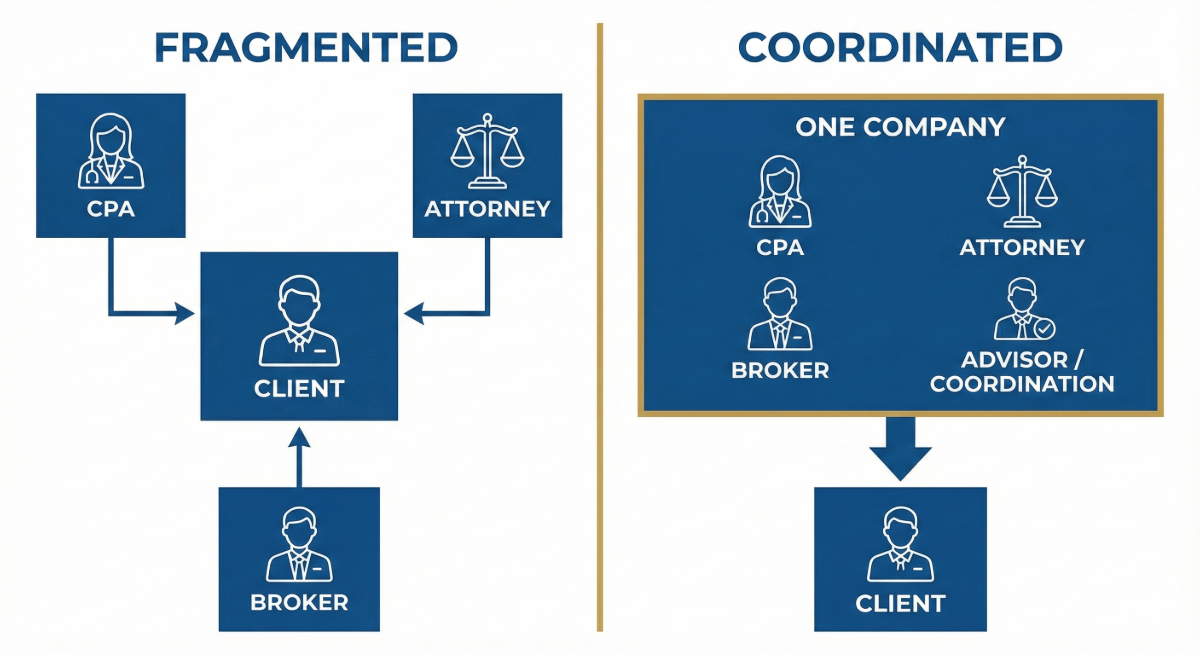

Team Versus Solo Practitioner

Consider whether you want to work with an individual advisor or a team. Both models have merits.A solo practitioner offers a single point of contact, but that also means their knowledge has limits and your relationship depends entirely on one person’s availability and tenure. A team brings diverse expertise and continuity.

For complex situations that require integration of tax planning, estate planning, and investment management, a team model often makes sense. No single person, regardless of credentials, can be an expert in everything. A team of specialists, including CPAs, certified financial planners, estate attorneys, and investment analysts, can address high-level needs more effectively than any sole individual.

Communication Style and Accessibility

You will be sharing sensitive information and making important decisions with this person or team. The relationship needs to work on a human level. Pay attention during initial conversations to how well they listen, whether they explain things clearly, and whether you feel comfortable asking questions or being honest about your situation.

Also, understand their service model. How often will you meet? How quickly do they respond to questions? Who will you actually be working with day to day? The world’s best expertise can only help if you can access it when you need it.

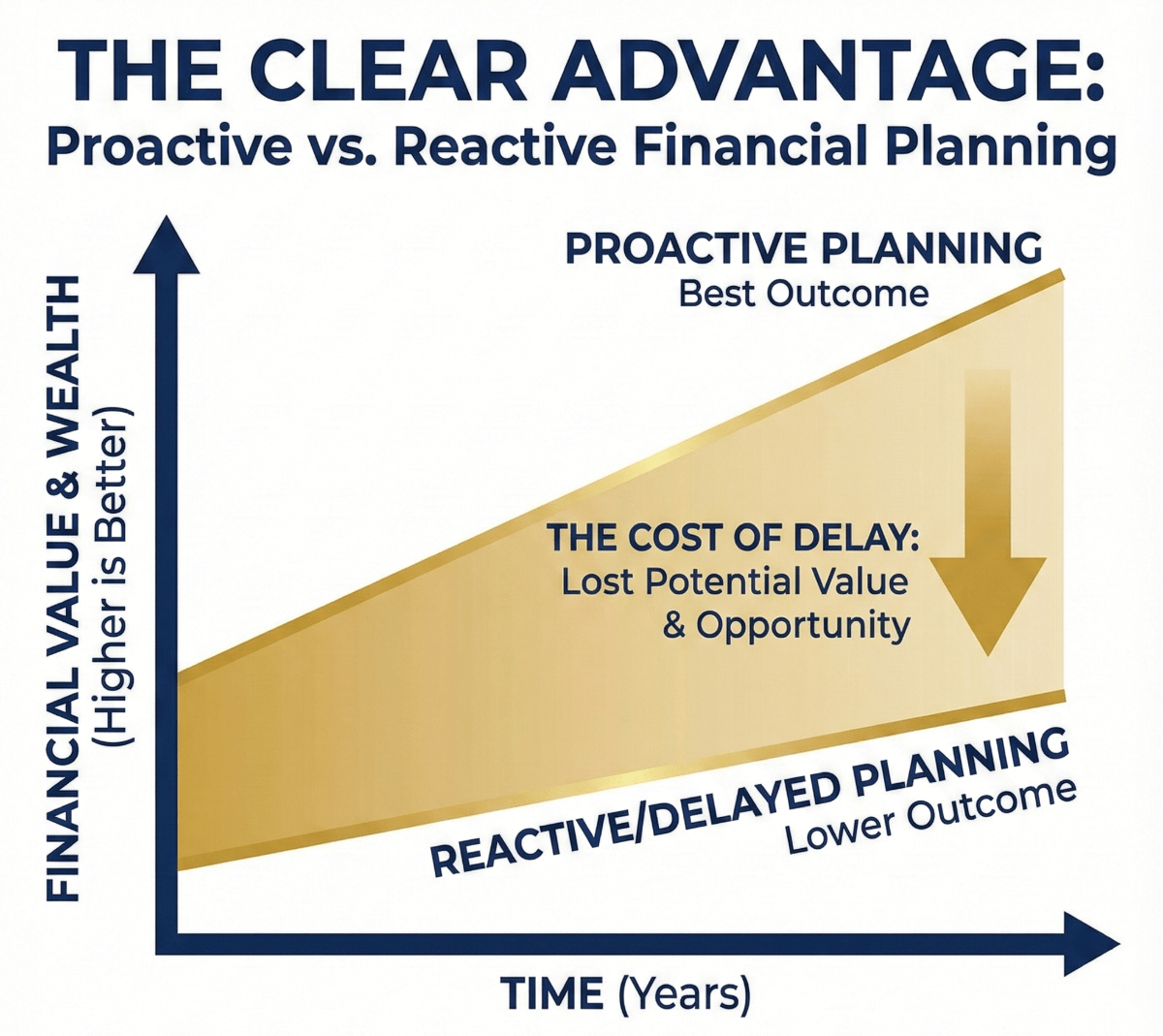

The Cost of Waiting Too Long

While this guide has emphasized that not everyone needs a financial advisor, it is equally important to address the opposite problem: waiting too long once your situation warrants wealth management.

The costs of delay compound over time. Suboptimal investment allocations create drag on your returns year after year. Tax inefficiencies add up. Estate planning gaps can result in significant consequences for your heirs. Missed opportunities become more expensive the longer they persist.

Many people put off engaging a financial advisor because they think they need to get their financial house in order first. This is backwards thinking. Getting your financial house in order is exactly what a good advisor helps you do. If your situation is complex enough to need help, waiting until it is less complex is not a realistic strategy. It will only become more complex over time.

The other common delay is waiting for some future milestone: a certain net worth, a promotion, retirement, or selling a business. While these events might trigger the need for different types of planning, the best time to engage is usually before the triggering event, not after. Planning done proactively creates better outcomes than planning done reactively.